Covar: shrinkage covariance estimation¶

This Python package contains two functions, cov_shrink_ss() and cov_shrink_rblw() which implements plug-in shrinkage estimators for the covariance matrix.

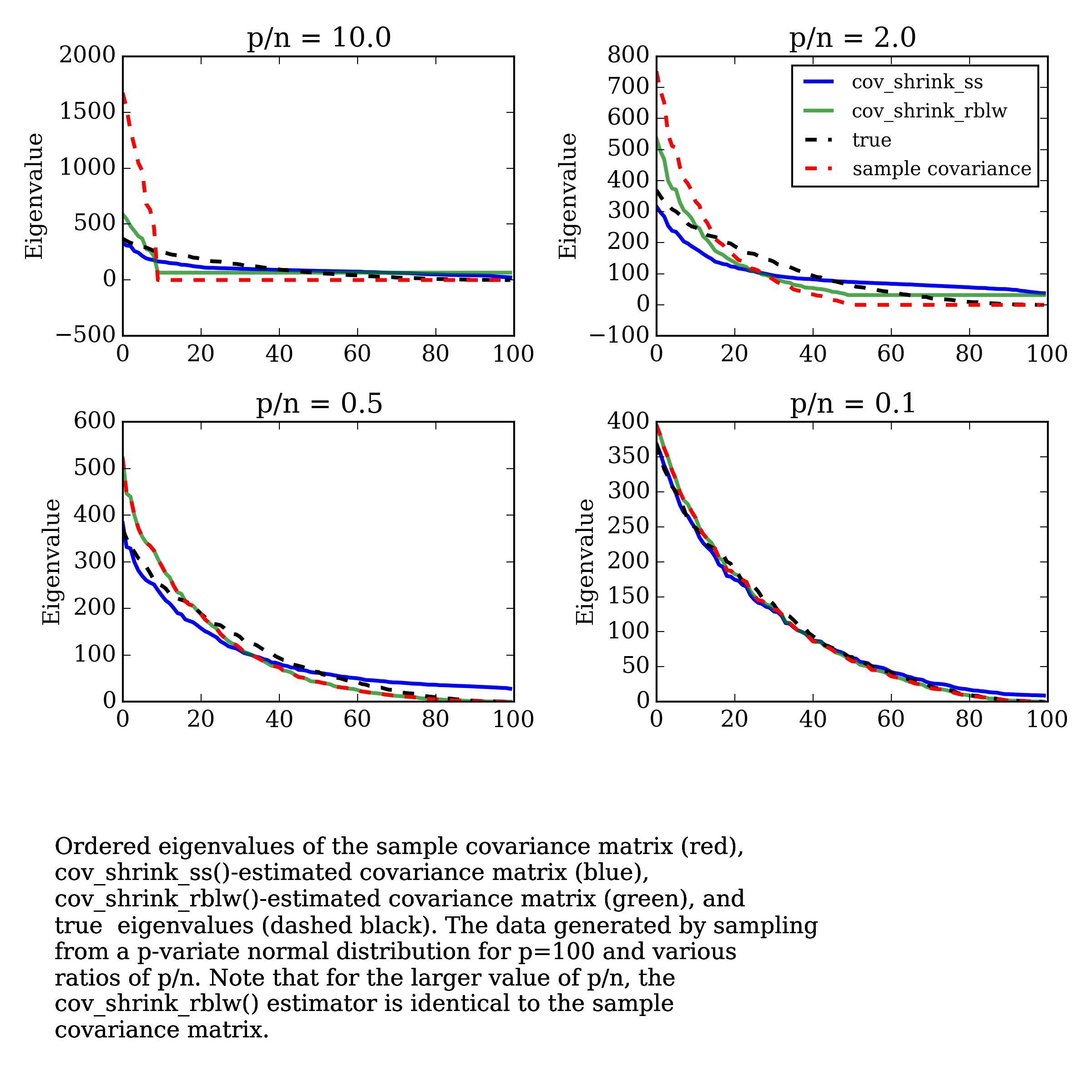

The cov_shrink_ss() estimator is described by Schafer and Strimmer (2005), where it is called “Target D: (diagonal, unequal variance)”. The cov_shrink_rblw() estimator is described by Chen Yilun, Wiesel, and Hero (2009).

Installation¶

$ pip install covar