Introduction¶

Get som arbitrary daily fund data from vanguard and ishares with pandas_datareader

(the usual imports are suppressed)

In [1]: start = datetime.datetime(2011, 1, 1)

In [2]: end = datetime.datetime(2016, 1, 1)

In [3]: f = data.DataReader(['VTWG', 'VBK', 'VONG', 'IUSG', 'IUSV',

...: 'VONV', 'VTWV', 'VIOV', 'IJK', 'IVOV'],

...: 'yahoo', start, end)

...:

In [4]: fsp = data.DataReader('^GSPC','yahoo', start, end) # S&P 500

In [5]: fsp = fsp['Adj Close'].pct_change().iloc[1:]

In [6]: rets = f['Adj Close'].pct_change().iloc[1:]

In [7]: rets = rets.apply(lambda x: np.log(1 + x))

In [8]: rets.head(5)

Out[8]:

IJK IUSG IUSV IVOV VBK VIOV \

Date

2011-01-04 -0.011640 -0.005500 -0.000811 0.000000 -0.011801 -0.017981

2011-01-05 0.005343 0.005500 0.005317 -0.003861 0.012180 0.003915

2011-01-06 -0.002668 0.000211 -0.002771 -0.000336 -0.002020 -0.006042

2011-01-07 -0.002278 -0.001266 -0.003590 -0.004215 -0.003925 -0.007398

2011-01-10 0.006623 0.001477 -0.001510 0.002700 0.007457 0.003459

VONG VONV VTWG VTWV

Date

2011-01-04 -0.004230 -0.000525 -0.017888 -0.016540

2011-01-05 0.005580 0.006113 0.008513 0.007239

2011-01-06 -0.002363 0.000522 -0.000942 -0.004107

2011-01-07 0.005057 -0.007687 -0.005989 -0.006109

2011-01-10 -0.003031 -0.001053 0.010536 0.001655

Construct a model object with an estimation window of 650 observations and a step size of 12 observations (i.e rebalancing every 12 days)

(these two parameters could be tuned with for ex. cross validation)

In [9]: from entroport import EntroPort

In [10]: ep = EntroPort(rets, 650, 12).fit()

Have a look at the cumulative return

In [11]: (ep.pfs_['ip'] + 1).cumprod().plot();

In [12]: (fsp[ep.pfs_.index[0]:] + 1).cumprod().plot().legend(['IP', 'SP500'], loc=2);

The estimated weights look reasonable (only point estimates are computed) but are noisy¶

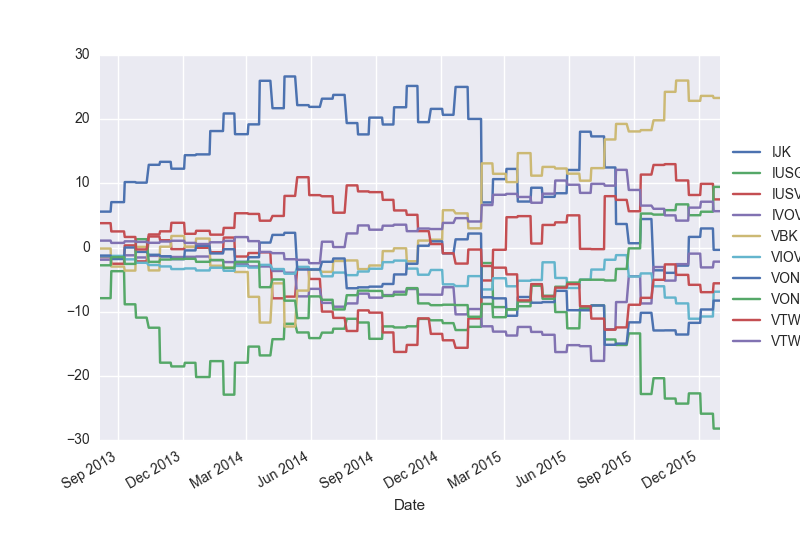

In [13]: ep.weights_.plot().legend(loc='center left', bbox_to_anchor=(1, .5));

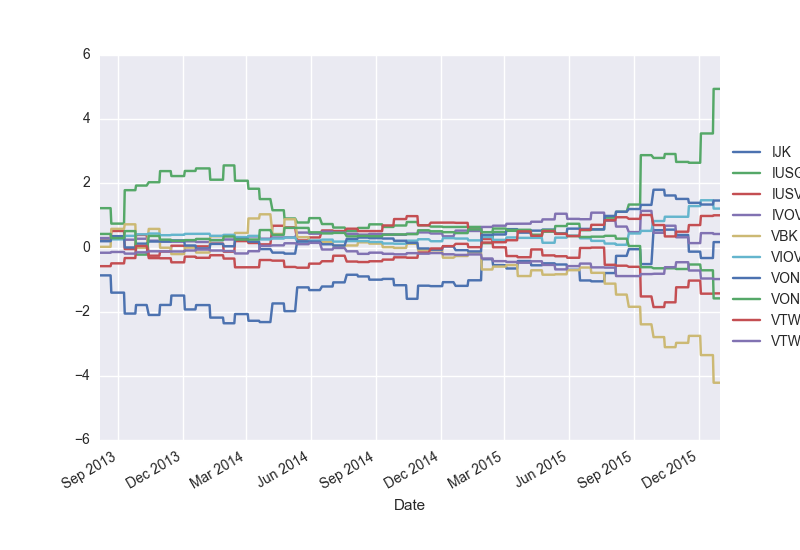

The estimated \(\theta_i\)‘s (the argmin of \(\frac{1}{T} \sum_{t=1}^{T}e^ {\boldsymbol{\theta}' \mathbf{R}_t}\))

In [14]: ep.thetas_.plot().legend(loc='center left', bbox_to_anchor=(1, .5));